Det finns mer än 400 000 försäkringsombud i detta land, och nästan alla av dem skulle älska att sälja en hel livförsäkring till dig. Om du köper en försäkring med premier på $40 000 per år, skulle provisionen vanligtvis vara någonstans mellan $20,000 och $44,000 för den agenten. Som du kanske föreställer dig kan den provisionen vara mycket motiverande, särskilt med tanke på medianinkomsten för försäkringsagenter på $49 840. För att göra saken värre erbjuder många av de sämsta policyerna de högsta provisionerna. Tyvärr säljs de allra flesta försäkringar som säljs på ett olämpligt sätt och den stora majoriteten av de som säljer den är säljare som utger sig för att vara finansiella rådgivare.

Som ett resultat av denna löjliga intressekonflikt kan agenter ofta kasta ut några allvarliga myter i ett försök att övertala dig att köpa deras produkt, vilket kan förklara den fördömande statistiken att 80 %+ av de som köper den här produkten blir av med den innan de dör och omröstningar av verkliga läkare på denna sida och vår Facebook-grupp visar att den stora majoriteten av dem som har köpt hela livets policy ångrar. Om detta är alla nyheter för dig, läs allt du behöver veta om hela livförsäkring innan du fortsätter med det här inlägget.

Medan de flesta WCI FB-gruppmedlemmar aldrig har köpt en hel livförsäkring, ångrar 76 % av dem som har det.

Laddar ...

Siffrorna är liknande men något lägre i den pågående omröstningen på denna sida (som till skillnad från FB-gruppen tillåter att röstning görs av de som säljer dessa policyer).

Många tror att jag hatar hela livförsäkringar. Det gör jag faktiskt inte. Jag hatar sättet det säljs och de som säljer det på ett olämpligt sätt. Om du verkligen förstår hur det fungerar och fortfarande vill ha det, köp gärna så mycket du vill. Det påverkar mig verkligen inte på ett eller annat sätt. Men jag är trött på att stöta på läsare och lyssnare som INTE förstod hur det fungerade när de köpte det, och när de väl förstår det, vill de INTE ha det.

Hellivsförsäkring kan sättas upp på många olika sätt, men i allmänhet betalar du en månatlig eller årlig premie för antingen en bestämd tidsperiod, eller tills du dör. Ju längre tid du betalar premierna desto lägre blir premierna. Närhelst du dör får din förmånstagare intäkterna från försäkringen. Eftersom varje livförsäkring garanterat kommer att betalas ut om du bara håller fast vid den till din död, är premierna mycket högre än en jämförbar livförsäkring.

En hel livförsäkring är, precis som andra typer av permanent livförsäkring, egentligen en hybrid av försäkring och investering. Försäkringen ackumulerar kontantvärde allt eftersom åren går. Det kontantvärdet växer på ett skatteskyddat sätt, och du kan till och med låna pengarna därinne skattefritt (men inte räntefritt). Vid din död tas allt du lånat (plus räntan) från dödsfallsersättningen, och resten betalas ut till din förmånstagare. (Du får kontantvärdet eller dödsfallsersättningen, inte båda.)

Denna investeringsaspekt gör att de som säljer en hellivsförsäkring kan hitta alla möjliga kreativa anledningar till att du bör köpa den och kreativa sätt att strukturera den. De mest extrema förespråkarna kanske till och med hävdar att du inte behöver NÅGRA andra finansiella produkter under hela ditt liv eftersom hela livförsäkringar uppenbarligen kan ta hand om alla dina behov inklusive bolån, konsumentlån, försäkringar, investeringar, universitetssparande och pension.

Problemet är att för varje användning av hela livförsäkringar finns det vanligtvis ett bättre sätt att hantera den ekonomiska frågan. Det här inlägget är de 38 vanliga myterna om hela livförsäkringar som sprids av dess förespråkare.

Hellivsförsäkring är inte det bästa sättet att skydda din inkomst, det är livsförsäkring. Innan du går i pension kan du köpa en billig livförsäkring för att ta hand om dina nära och kära i händelse av din förtida död. En livförsäkring på 30-årsnivå och med ett nominellt värde på 1 miljon USD köpt på en frisk 30-åring kostar 680 USD per år. En liknande försäkring för hela livet kommer att kosta mer än 10 gånger så mycket, $8 000-$10 000 per år. Det är pengar som inte kan spenderas på bolånebetalningar eller semester, och inte heller investeras för pensionering.

Hela livet är inte det bästa sättet att få en permanent dödsfallsersättning – garanterat universellt liv utan förfallotid. Det finns ett fåtal utvalda personer som behöver eller vill ha en försäkring som betalas ut vid deras död, när det än må vara. Detta kan vara användbart för vissa ovanliga fastighetsplaneringsfrågor. Men det finns en bättre produkt som ger detta och är mycket billigare än en hel livförsäkring. Den kallas Garanterad, förfallen universell livförsäkring . Det samlar INTE något kontantvärde utan ger helt enkelt en livslång dödsfallsersättning. Det kostar bara hälften så mycket som en hel livförsäkring, så du kommer inte bli förvånad över att få reda på att agentens provision på denna försäljning kommer att vara mycket lägre.

Kalla mig cynisk, men jag misstänker att det kan vara en av anledningarna till att du aldrig har hört talas om ett garanterat universellt liv utan förfallotid. Hela livförsäkringen ger en garanterad dödsfallsersättning som PROJEKTERAS (men inte garanterad) kommer att växa långsamt så att om du dör under din förväntade livslängd eller senare kommer du att lämna efter dig lite mer än den ursprungliga försäkringsersättningen vid dödsfall.

En policy för hela livet som jag tittade på nyligen beräknade dödsfallsförmånen för en försäkring på 1 miljon dollar, köpt vid 30, skulle vara 3,17 miljoner dollar vid dödsfall vid 83 års ålder. Det låter bra, nästan som ett inflationsskydd för dödsfallsersättningen. Förutom att den historiska inflationen är ungefär 3,1%. Med 3,1 % skulle 1 miljon dollar nu motsvara 5,04 miljoner dollar på 53 år. En politik för hela livet skulle förstöras av oväntad inflation, eftersom utdelningarna i första hand backas upp av nominella obligationer, vars värden skulle mördas i en miljö med hög inflation.

Därför är hellivsförsäkring varken det bästa sättet att ge en garanterad livslång nominell dödsfallsersättning eller en garanterad livslång real dödsersättning. Så vad är det bra för? Vad sägs om en garanterad dödsfallsersättning som kan komma att öka om försäkringsbolaget känner för att öka den? Skulle du vara villig att betala dubbelt så höga premier för det? Jag trodde inte det.

Hela livet är inte det bästa sättet att investera – traditionella investeringar är det. När du betalar hela livets premier går en del av pengarna till att köpa försäkring, en del av dem går till omkostnader och vinst för försäkringsbolaget, och en del av det går till provision för säljaren. Resten går sedan till kontantvärdedelen av försäkringen.

Varje år deklarerar försäkringsbolaget en utdelning, och om det finns $10 000 i kontantvärdedelen och utdelningen är 6%, så krediteras $600 till ditt kontantvärde. Utdelningen tillämpas endast på kontantvärdet, inte hela premien som betalas, så den genomsnittliga utdelningsräntan är inte på något sätt, form eller form relaterad till din faktiska avkastning på försäkringen som en investering. Faktum är att avkastningen på investeringen i allmänhet är negativ under minst ett decennium. Jag analyserade nyligen en policy för en frisk 30-årig man med en förväntad livslängd på 53 år. Den garanterade avkastningen på kontantvärdet var mindre än 2 % per år EFTER 5 DECENADER .

Även om du använder försäkringsbolagets optimistiska "prognostiserade" värden, ser du fortfarande på en avkastning på mindre än 5%. I verkligheten kommer du förmodligen att få en avkastning på 3%-4%. Med tanke på att du måste hålla fast vid denna "investering" i 5 decennier, verkar det inte som mycket kompensation. Om du har decennier att investera är det mycket klokare att ta mer risk med dina investeringar och tjäna en högre avkastning. En investering i aktier eller fastigheter kommer sannolikt att ge en avkastning under decennier i intervallet 7%-12%. 100 000 USD investerade i 50 år med 3 % per år kommer att växa till 438 000 USD. Om den istället växer med 9 % kommer du att få 7,4 miljoner dollar, eller 17 gånger så mycket pengar. Hur snabbt du kombinerar dina långsiktiga investeringar spelar roll, särskilt över långa tidsperioder.

Vissa agenter tror att försäkringsbolag på något sätt kan få investeringsavkastning som du eller jag inte kan hitta någon annanstans och förmedla den stora avkastningen till sina försäkringsägare. Det kan vara belysande att titta under huven och se vad som verkligen finns i ett försäkringsbolags portfölj. Under 2016 investerades försäkringsbolagens tillgångar 67 % i obligationer (nästan alla i löpande företags- och statsobligationer), 1 % i preferensaktier, 12 % i stamaktier, 8 % i bolån, 1 % i fastigheter, 4 % i kontanter, 2 % i lån till sina försäkringsägare i ”och andra cirka 5 %”. Tack vare indexfondrevolutionen kan en enskild investerare köpa nästan allt det där för mindre än 10 punkter per år i utgifter. Aktiv förvaltning fungerar inte bättre för försäkringsbolag än för fonder.

Som du kanske förväntar dig är avkastningen på en portfölj som huvudsakligen består av statsobligationer (avkastar för närvarande 1%-2%) och företagsobligationer (för närvarande ger en avkastning 3%-4%) inte särskilt hög. Så var kommer utdelningen ifrån? En del kommer från avkastningen på investeringsportföljen, en del kommer från avgifterna för dem som överlämnade sina försäkringar, och en del kommer från "dödlighetskrediter", vilket i princip är pengar de inte behövde betala ut till förmånstagarna eftersom färre människor dog än de planerat för (dvs. du betalade för mycket för försäkringsdelen av försäkringen i första hand på grund av statliga regler). Det finns inga magiska investeringar som försäkringsbolag kan investera i som du inte kan utan bolaget. Varje ytterligare lager mellan dig och investeringen ökar bara utgifterna och sänker avkastningen.

Det finns massor av tillgångsklasser värda att inkludera i en diversifierad portfölj, men hela livet är inte en av dem. Försäkringssäljare tar i allmänhet till detta argument när de har insett att de inte kan övertyga dig om att hela livet är en stor investering i sig. De säger att om du blandar det i en portfölj av aktier, obligationer och fastigheter kommer det att förbättra den övergripande portföljen. Däremot kan du kalla allt du vill för en tillgångsklass. Hästgödsel kan vara en tillgångsklass, men det betyder inte att du ska investera i det. Tänk på det så här. Om jag sa att jag hade en tillgångsklass med följande egenskaper:

skulle du köpa den? Naturligtvis inte.

Hela livet är inte det bästa sättet att sänka din investeringsskatt, det är pensionskonton. Många agenter gillar att presentera skattefördelarna med en hellivsförsäkring, och jämför det ofta med en 401(k) eller en Roth IRA. Kontantvärdet växer på ett skatteskyddat sätt, kontantvärdet kan lånas skattefritt och intäkterna från försäkringen vid din död är inkomst (dock inte dödsbo) skattefria. Så vissa förespråkare för hela livet föreslår att du använder en hellivsförsäkring istället för ett pensionskonto som en 401(k) eller en Roth IRA. Men en 401(k) eller Roth IRA ger inte bara MER skattebesparingar och låter dig investera i mer riskfyllda investeringar som sannolikt kommer att ge dig en högre avkastning, men du behöver inte heller låna dina egna pengar eller betala ränta för förmånen att göra det.

Jag har tidigare skrivit om de 3 sätten en 401(k) sparar dig på skatter och om hur hela livförsäkringen inte är som en Roth IRA. Jag har också skrivit om hur skatteeffektiva investeringar i ett skattepliktigt investeringskonto inte bär nästan samma skattebörda som agenter vill säga att de gör. Finns det skattefördelar med att investera i livförsäkring? Ja, men de är dramatiskt översålda.

Försäkringsagenter älskar att använda den här på läkare, som kan vara paranoida när det gäller problem med tillgångsskydd. Men de nämner ofta inte (eller kanske ens vet) att lagar om tillgångsskydd är mycket statliga. Till exempel [2022] , i Alabama, är endast $500 av hela livförsäkringens kontantvärde skyddad från borgenärer, men 100% av pengarna i din 401(k) eller IRA är skyddade. West Virginia ger bara ett skydd på $8 000. South Carolina skyddar 4 000 dollar. New Hampshire ger inget skydd. Många stater ger 100 % skydd för hela livförsäkringens kontantvärde, men du borde antagligen leta upp din delstats specifika lagar innan du faller för denna myt.

Livförsäkring med kontantvärde har några fantastiska funktioner för fastighetsplanering som kan vara mycket användbara. Men de allra flesta människor, inklusive läkare, behöver inte dessa funktioner. Den primära fördelen med livförsäkring är att du får ett gäng inkomstskattefria pengar vid din död. Detta kan hjälpa till med många likviditetsfrågor, såsom ägande av dyr fastighet eller en privat verksamhet. Om du har två barn som du vill dela lika på din egendom, och det mesta av din egendom är familjegården, måste de antingen sälja gården, dela den på mitten eller låta det ena köpa ut det andra för att dela lika. Men om du också hade en livförsäkring med samma värde som gården, kunde den ena ungen få gården och den andra få försäkringsintäkterna. På samma sätt, i det lyckosamma fallet att du har en mycket stor egendom (mer än 5 miljoner dollar för ensamstående i den federala skattelagen, men kan vara mycket mindre i vissa stater), kan livförsäkringsintäkterna användas för att betala fastighetsskatten. Detta skulle vara användbart även med en ensam arvtagare för att hindra honom från att sälja en värdefull fastighet eller verksamhet till brandförsäljningspriser för att betala skatteräkningen.

Vissa människor gillar också att sätta livförsäkring i ett oåterkalleligt förtroende för att minska storleken på sin egendom och undvika fastighetsskatter. Även om du kan lägga enkla skattepliktiga investeringar i trusten istället (och sannolikt skulle komma framåt på grund av högre avkastning), kan förtroendeskattesatserna vara ganska höga, vilket drar tillbaka avkastningen för skatteineffektiva investeringar, för att inte tala om krångelfaktorn. Det är viktigt att påpeka att det inte är livförsäkringen som sparar pengar på fastighetsskatt, det är det faktum att du ger bort dina tillgångar innan du dör genom att lägga dem i förtroendet.

Faktum är dock att den stora majoriteten av amerikaner, till och med läkare, och till och med inklusive läkare med ett "fastighetsskatteproblem", inte behöver en hel livförsäkring för att göra effektiv fastighetsplanering. De flesta människor kommer att dö utan någon fastighetsskatt. Av dem vars dödsbon kommer att vara skyldiga vissa fastighetsskatter har de allra flesta likvida medel som kan användas för att betala skatterna. Även om du vill minska storleken på din dödsbo för att förhindra fastighetsskatt kan du enkelt göra det utan att köpa livförsäkring. Du och din make kan ge $16 000 vardera [2022 — besök vår sida med årliga siffror för att få de senaste siffrorna] till någon arvinge under ett givet år utan några arvs-/gåvoskattekonsekvenser. Som ett exempel, om du hade 4 barn och de hade 4 barn vardera och alla 20 arvingarna var gifta, är det 40 personer. 40 x 16 000 USD x 2 =1,28 miljoner USD per år som kan tas ut från din egendom utan att betala några fastighets-/gåvoskatter. Det tar inte lång tid att komma under fastighetsskattegränsen i den takten, ingen försäkring behövs.

Vissa agenter går till och med så långt att de föreslår att du använder en policy för hela livet för att betala för dina barns college. Kan du göra det här? Naturligtvis. Du tar helt enkelt policylån och skickar de pengarna till universitetet för att betala undervisningen. Men du är bättre att spara till college med en bra 529 av flera skäl. För det första får du ofta en statlig skattelättnad genom att använda en 529 som inte är tillgänglig för hela livförsäkringar. För det andra behöver du inte låna pengar från din 529, du bara tar ut dem. Inga räntebetalningar krävs. Sist, men absolut inte minst, överväga tidsramen för college-besparingar. Föräldrar sparar i allmänhet till college under en period på 5-20 år. Genom att investera de pengarna aggressivt kan de förvänta sig en avkastning på 7%-10%. Hela livförsäkringar har mycket dålig avkastning under tidsperioder på mindre än 20 år. Faktum är att många gånger är kontantvärdets avkastning på din "investering" under hela livet negativ under minst ett decennium. Det är viktigt att se till att dina pengar fungerar lika hårt som du gör, och att dina pengar är på semester under det första decenniet i en policy för hela livet. Hela livets förespråkare kommer att påpeka att om du dog, kan dödsfallsersättningen fortfarande betala för Juniors college, men det är mycket billigare att täcka den risken med livstidsförsäkring.

Försäkringsagenter kommer då och då att falla tillbaka på detta argument när det har påpekats att en klient egentligen inte har något behov av en permanent dödsfallsersättning. De medger att kunden faktiskt inte behöver en hel livförsäkring. Sedan försöker de sälja den utifrån att ha den som statussymbol eller lyx. "Visst, du behöver det inte, det är en lyx." En lyx är per definition något du inte behöver. Jag föredrar att min lyx är något som jag verkligen tycker om. Så innan du köper en hellivsförsäkring som en lyx, fråga dig själv, "Vad tycker jag verkligen om?" Om det är att äga en hel livförsäkring, okej, köp några. Men jag slår vad om att de flesta av oss skulle föredra en lyx som en fin bil, en kryssning med barnbarnen, eller kanske en donation till en välgörenhetsorganisation.

Hela livet är inte det bästa sättet att se till att du inte får slut på pengar, att livränta några av dina tillgångar är. Hela livet är inte det bästa sättet att ta itu med den andra att dö-frågan, korrekt strukturering av pensioner och livräntor är. Hela livet agenter gillar att komma med pensionsscenarier som får dig att känna att du måste äga eller åtminstone vill äga en permanent livförsäkring, särskilt för ett gift par. Till exempel kommer de att prata om en pension som bara betalas ut tills den arbetande maken dör. Eller så kommer de att prata om att göra en del av dina tillgångar livränta baserat på livet för endast en medlem av paret. Sedan kommer de att föreslå att intäkterna från hela livsförsäkringen används för levnadskostnader av den näst döende maken. Det finns ingen anledning att använda en hel livspolicy på detta sätt. Om du vill att din pension ska gälla tills ni båda dör, välj det alternativet. Om du vill att din livränta ska pågå tills ni båda dör, välj det alternativet. Ja, det kommer att betalas ut till en något lägre procentsats, men skillnaden mellan utbetalningarna är mindre än kostnaden för en hel livförsäkring som skulle täcka förlusten av den pensionen. Det är helt enkelt inte den rätta lösningen på problemet. Ger en hel livförsäkring viss flexibilitet vid pensionering? Visst, men kostnaden för den flexibiliteten är för hög.

Hela livet är inte det bästa sättet att köpa dyra grejer, att spara till det är det. Det finns några riktigt kreativa försäkringssäljare där ute som förespråkar system som Bank on Yourself eller Infinite Banking. Grundschemat är detta:genom att strukturera din försäkring på ett lämpligt sätt med betalda tillägg får du mycket kontantvärde i din försäkring under de första åren, så att du bryter jämnt på 3-4 år snarare än 8-15 år. Du köper också en policy som är "icke-direkt erkännande." Det betyder att när du lånar från försäkringen, fortsätter försäkringsbolaget att betala utdelning på det belopp som fanns där innan du lånade ut det, så försäkringsutdelningarna tar i princip ut räntebetalningarna på lånet. Nu, istället för att gå till ditt sparkonto eller till en bank för att låna pengar när du behöver en bil, ett kylskåp eller en investeringsfastighet, lånar du från hela din livsförsäkring i princip utan kostnad. Dessutom kommer kontantvärdet i försäkringen som du inte lånar att växa snabbare än pengarna i en sparbank.

Så vad är problemet? Problemet är att du måste köpa en hel livsförsäkring du inte behöver. Du kanske går sönder tidigare än vad du skulle göra med en traditionell policy, men det finns fortfarande flera år av negativ avkastning och på lång sikt samma låga avkastning. Är det bättre att tjäna 4%-5% per år efter 5 år eller tjäna 1% per år från och med år 1? Tja, under de första 6 eller 7 åren har du det bättre med ett sparkonto på 1 % per år. Dessutom, om räntorna går upp från sina historiska låga nivåer, är du fortfarande låst till detta system för resten av ditt liv. Det var inte särskilt länge sedan jag kunde få över 5% från en penningmarknadsfond. Det verkar också vara väldigt enkelt att finansiera en bil hos en återförsäljare till extremt låga räntor. 0 % eller 1 % är inte ovanligt. Det är bättre att du lånar från dem till 1 % än från din försäkring till 5 %. Det är ett liknande problem med vitvaror och bolån. Du går igenom allt det här så att du kan låna av dig själv och inser sedan att det är billigare att låna av någon annan. Slutligen, om du inte behöver göra ett köp på 5 eller 10 år, har du tid att investera i något som sannolikt kommer att ha en mycket högre avkastning än en försäkring för hela livet. Blir de som bankar på sig lurade? Inte nödvändigtvis, men de är i allmänhet översålda på grund av fördelarna med deras system. Dess förespråkare är främst försäkringsagenter som vill öka försäljningen genom kreativ marknadsföring. Att spara är helt enkelt ett bättre sätt att göra stora inköp än att köpa en försäkring för hela livet.

Hela livets förespråkare, särskilt de som förespråkar att du använder din policy som en bank, vill påpeka att många mycket rika människor och massor av företag (inklusive banker) faktiskt köper en hel livförsäkring. Även om det är sant, är det irrelevant för den typiska personen. Stora företag har inte tillgång till de skattebesparande pensionskontoalternativen som en medelklassindivid har. Ultrarika individer har redan maxat dessa. När du har mycket mer pengar än du någonsin kan behöva, spelar avkastningen på dina pengar inte så stor roll. Bill Gates har råd att investera i något som ger en avkastning på 2%-5% eftersom han inte behöver sina pengar för att jobba särskilt hårt. Det är helt enkelt inte sant för den stora majoriteten av medel- till överklassmänniskor, inklusive läkare. Som diskuterats ovan har ultrarika människor också mer användning för de begränsade fördelarna med fastighetsplanering och tillgångsskyddet med permanent livförsäkring. Kort sagt, den låga avkastningen som är inneboende i hela livet är mycket mindre ett problem för dem än för dig.

Försäljare för hela livet vill påpeka att hela livet är mycket billigare om du köper det när du är ung. Även om det är sant att premierna är lägre om du köper en försäkring vid 25 än om du köper den vid 55, när du tar hänsyn till pengars tidsvärde och det faktum att du kommer att betala premierna i 3 extra decennier, är det inte bättre av en investering i ung ålder än vid en äldre ålder. Aktuarier är mycket intelligenta människor, och för en risk som är relativt lätt att modellera, som dödsfall, kan de prissätta försäkringar ganska effektivt.

Förutom de lägre premierna finns det två andra anledningar till att det verkar bättre att köpa det när du är ung. För det första sprids den provisionen ut över fler år, så den har mindre inverkan på din totala avkastning. Men alternativet att inte betala provisionen alls är mycket mer attraktivt. För det andra är det möjligt att du antingen blir mindre frisk eller ägnar dig åt någon farlig sport senare i livet. Detta är en av de allvarliga nackdelarna med att använda livförsäkring som en investering - alla kan inte använda den. Antingen kvalificerar de sig inte för det alls, eller så är priset på försäkringen så högt att avkastningen på investeringen är ännu lägre än de annars skulle vara. Jag ser det inte som en anledning att köpa den när man är ung, jag ser det som en anledning att inte köpa den alls. Kan du föreställa dig om Vanguard skickade ut en ambulanspersonal till ditt hus för att ta blod innan de låter dig köpa deras S&P 500-fond?

Hellivsförsäkring är inte det bästa sättet att skydda din pensionsinkomst från ditt funktionshinder, det är sjukförsäkring. Försäkringsbolagen insåg att hela livförsäkringspremier är riktigt dyra och skulle vara svåra att göra i händelse av funktionshinder, började försäkringsbolagen erbjuda en ryttare som avstod från premierna i händelse av ditt funktionshinder. Ibland verkar du inte ens behöva betala extra för denna förmån. De som faller för denna taktik saknar ett par poäng. För det första är garantier inte gratis. Varje garanti kostar dig pengar i form av lägre avkastning, oavsett om försäkringsbolaget tar extra betalt för garantin eller "bakar in det i försäkringen" så att det döljs.

För det andra är sjukförsäkringen komplicerad och definitionen av funktionshinder är viktig. De flesta läkare som vill ha handikappskydd spenderar mycket pengar på att få en riktigt bra försäkring med en bred definition av funktionshinder inklusive täckning för "eget yrke", eftersom de vill se till att företaget kommer att behöva betala i händelse av deras funktionshinder. De ryttare som säljs på hela livets policyer är inte alls lika omfattande och är mycket mindre benägna att få betalt i de många gråzoner som funktionshinder ofta hamnar i. Du kommer med största sannolikhet att bli bättre av att köpa en större handikappförsäkring snarare än ett helt livsavstående från premiumryttare. Din handikappförsäkring kan också erbjuda en pensionsskyddsryttare. Även om dessa också har problem (främst i sättet som förmånen betalas ut), är de bättre än att försöka få din sjukförsäkring från en livsförsäkring.

Om du planerar en förtidspension som jag, kanske du inser att du inte behöver din handikappskydd för att skydda dina pensionsavgifter ändå, åtminstone efter några år av tungt sparande. Överväg att ha en portfölj på 750 000 USD vid 40 års ålder. Du tror att du behöver 2 miljoner USD i dagens dollar för att gå i pension. Du planerar att spara stort så att du kan uppnå det vid 50 års ålder och gå i pension. Vad är reservplanen om du blir funktionshindrad och inte kan spara alla de pengarna? Din sjukförsäkring betalar sig inte bara till 50 års ålder. Den betalar sig till 65 år. Så du behöver inte din portfölj för att täcka dessa 15 år. Du kan också börja få sociala avgifter när invaliditetsersättningarna tar slut. Eftersom du inte behöver röra din portfölj kan den fortsätta att växa. Om den växer med 5 % efter inflationen kommer den att vara värd över 2,5 miljoner USD i dagens dollar när du fyller 65 år. Köp inte en försäkring som du inte behöver. Men redan innan du har någon form av portfölj är det bästa sättet att skydda ditt pensionssparande att köpa MER sjukförsäkring, inte att försöka få det från en hel livsförsäkring. Även om du skulle kunna använda den extra täckningen för att tillhandahålla din pensionsportfölj, måste du kunna sätta in den i en investering med hög avkastning, vilket hela livet är osannolikt att ge. Ett aggressivt investerat skattepliktigt konto är bara bra eftersom din huvudsakliga inkomst om du är funktionshindrad, dina sjukförsäkringsförmåner, är skattefria.

Eftersom en agent får en ny provision varje gång han säljer en ny försäkring, även om han ersätter en gammal från samma företag, har han en allvarlig intressekonflikt när det gäller att ge rekommendationer till dig. Jag interagerar med massor av försäkringsagenter på den här bloggen, och ingen av dem håller med de andra om vad en "korrekt strukturerad" livspolicy är. Det betyder att om du går till en andra agent kommer han nästan säkert att berätta att det finns ett bättre sätt att göra det. Men för att det ska löna sig att byta ut en politik mot en annan måste den ursprungliga politiken vara helt fruktansvärd, särskilt efter ett par decennier. Anledningen till detta är att den dåliga avkastningen på hellivsförsäkring är koncentrerad till de första åren. Jag tittade nyligen på en policy. Denna sattes upp som en investering med inbetalda tillägg under de första 25 åren. Det var agentens bästa försök att maximera avkastningen på en policy. Så här såg den årliga avkastningen ut:

Garanterat Projicerat Första 10 åren-1,84%0,98%Nästa 15 år2,55%5,47%Nästa 25 år1,99%5,13%Detta visar att den dåliga avkastningen är mycket koncentrerad till de första åren. Med just denna policy minskar faktiskt avkastningen efter 25 år eftersom det är då du slutar göra inbetalda tillägg. Med en mer traditionell policy skulle den tredje raden vara något högre än den andra raden. Men moralen i historien är att du ska köpa "rätt policy" först, och även en skitpolitik som är mer än 10 år gammal kommer att bli bättre än en helt ny bättre politik. Detta är också anledningen till att det kan vara en bra idé att behålla en äldre livspolicy, även om det var ett misstag att köpa den från början. Det är också anmärkningsvärt att se hur liten risk försäkringsbolaget faktiskt tar, eftersom det inte ens är en garanti för att ditt kontantvärde kommer att hålla jämna steg med inflationen.

Hela livet är inte det enda sättet att skicka pengar till arvingar inkomstskattefritt vid din död. I själva verket är det inte ens det bästa sättet, en Roth IRA är. När du avlider får dina arvingar en försäkringsersättning vid dödsfall som är fri från inkomstskatt. Vad agenter ofta misslyckas med att nämna är att nästan allt dina arvingar får från dig när du dör är inkomstskattefritt. Tack vare den ökade grunden vid dödsfall omvärderas allt utanför ett pensionskonto, inklusive möbler, bilar, aktier, kontanter, fonder och fastigheter på dagen för din död. Eftersom underlaget nu är detsamma som värdet, utgår ingen kapitalvinstskatt. Att ärva ett pensionskonto kan vara ännu bättre, speciellt ett Roth-konto där skatterna redan är betalda. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

Are you kidding me? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

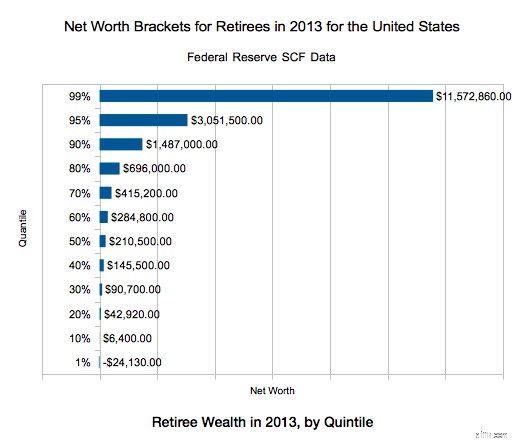

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

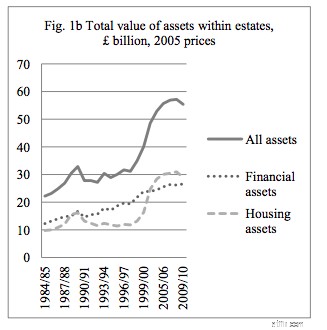

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Där går du. Forty reasons for buying whole life insurance debunked. Don't worry; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Have more questions about life insurance and what kind of policies would be best for you? Hire a WCI-vetted professional to help you sort it out.

Agree? Disagree? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.

Måste jag kräva IRA-ränta på mina skatter?

Hur man räknar ut nettominskningen i kontanter

Hur man köper Decentraland-tokens (MANA)

Aflac Dataintrång:Kunder som potentiellt drabbas av cyberattacker i hela branschen

Låt inte oväntade skatter förminska dina pensionsdrömmar

Billån för dålig kredit &ingen kredit - bli godkänd | [Ditt företagsnamn]

Hur man använder dubbla kuponger

Är 4,2 miljarder dollar rimligt? Hur man utvärderar Instacarts värdering