Tycker du att en livförsäkring för miljoner dollar låter som för mycket försäkring?

Som Certified Financial Planner ser jag underförsäkrade personer varje dag.

Vad ska jag säga till dem?

En livförsäkring på miljon dollar kan faktiskt vara den minsta täckning som behövs för ett typiskt medelklasshushåll, men det är överkomligt.

Det kan låta som en överdrift, men om du krymper siffrorna – precis som vi kommer att göra lite – kommer du att inse att en miljondollarpolitik kan vara mycket rimlig.

Den goda nyheten är att livstidsförsäkring inte är så dyr som de flesta tror.

Det som gör terminen ännu bättre är att större försäkringar kostar mindre i promille än vad mindre försäkringar gör. Du kanske upptäcker att premien på en försäkring på 1 miljon USD bara är lite högre än den är för 500 000 USD.

I den här resursen:

Med en livförsäkring kan du ta hand om din familj på rätt sätt. Skulle något hända dig, kommer du att vilja lämna dina nära och kära ett ekonomiskt ägg för deras välbefinnande. Klicka på ditt tillstånd för att ta reda på mer. Get Started

Med en livförsäkring kan du ta hand om din familj på rätt sätt. Skulle något hända dig, kommer du att vilja lämna dina nära och kära ett ekonomiskt ägg för deras välbefinnande. Klicka på ditt tillstånd för att ta reda på mer. Get Started Probably, but lets find out. A general rule of thumb that many life insurance companies use is around 10 times your income. If you’re young, that may be low because you may want to provide your family with enough to replace your income for 15 years or more.

Today, $1 million has become the new baseline for life insurance by a primary breadwinner. Anything less could leave your family financially impaired.

Here’s a list of all the different obligations you may want to have life insurance cover in the unfortunate event you pass away early.

Now that you have an idea of these obligations, let’s punch them into this life insurance calculator to find out if you need a million dollar policy.

According to Policy Genius, the average cost for a $1,000,000, 20-year term life insurance policy for a 35-year-old male is $53 per month. However your rate will vary according to the following factors.

Factors that affect your rate:

The best, and easiest place to start is online. I recommend having two or three insurers compete for your business to make sure you get the best rate and coverage.

To get started seeing how cheap term life can be, choose your state from the map below to instantly be matched with top life insurance providers.

Let’s look at the individual components that can quickly add up to over a million dollar policy.

This is where things can get a bit intimidating. Even if you earn a modest income, you may need close to $1 million to replace that income after your death.

The conventional wisdom in the insurance industry is that you should maintain a life insurance policy equal to between 10 times and 20 times your annual income.

If you earn $50,000 per year, that would mean a policy of between $500,000 and $1 million.

The complication today is that with interest rates being as low as they are that might not be enough either.

For example, if you have a $1 million policy that could be invested at 5% per year, your family could live on the interest earned – which conveniently comes to $50,000 per year – for the next 20 years.

That would still leave the original $1 million intact to cover other expenses. But with today’s microscopic interest rates, there’s no way to get a guaranteed return of 5% on your money, certainly not for 15 or 20 years.

That brings us back to simple math – multiplying your annual income times the number of years your family’s living expenses will need to be covered. This alone can require a $1 million life insurance policy.

Here we start with the basics – wrapping up your final affairs.

This will include funeral costs and any lingering medical costs. A reasonable estimate for a typical funeral is around $20,000.

Crazy, right? You can get burial insurance to cover only the most basic of final expenses.

Debt burdens are high in the US, and debt can be especially crushing on remaining family members. Many life insurance customers make sure they can pay off most of their debt with the policy.

Medical Debt

Medical costs are a serious variable. Even if you have excellent health insurance, there are likely to be unpaid medical bills lingering after your death. This has to do with copayments, deductibles, and coinsurance provisions.

Collectively, they can add up to many thousands of dollars. But where things get really complicated is if you die of a terminal illness.

For example, if you are stricken by an illness that lasts for several years, you could incur a number of expenses that are not covered by insurance. This may include the cost of personal care and even experimental treatments.

Mortgage

A home may be a large asset, but it’s also often a homeowner’s largest debt. The average mortgage balance in the US is roughly $202,000 according to Experian data. So you could easily use a life insurance policy to pay off that debt and relieve your loved ones of a monthly mortgage payment.

Personal Debt

Credit card debt and other personal debt are some of the most expensive obligations carrying rates upward of 20% in some cases. Make sure you have enough to cover this very expensive debt.

Below is a sampling of major expenses your family is likely to incur, either on an annual basis or at some point after your death.

College

College costs continue to skyrocket. The Department of Education suggests that four year public college tuition has been rising an average of 5% per year, far exceeding the rate of inflation. If you have one child who attends an in-state public school, a second at an out-of-state public school, and a third in a private university, the total expenditure will reach $416,560.

Transportation

Vehicles and other forms of transportation represent another large sum. Unfortunately, with increasing electronics and safety features, the average cost of a new car continues to grow.

Health Insurance

If your family relies on your work for healthcare, take notice. Average health insurance premium for a family is $19,616. That’s a shade under $2,000 per month in additional cost. This cost will only rise, and the need could last for years.

So far, we’ve been describing the financial obligations likely to affect a typical household.

But there may be certain situations that will produce obligations that are less obvious.

Business Owner

For example, if you’re a business owner, there may be debts or other financial obligations that will need to be paid upon your death.

Even though no one in your family may be qualified or interested in taking over your business, the payoff of those obligations may be completely necessary to enable the sale of the business.

Real Estate Investor

Another possibility is that you’re a real estate investor.

If your properties are heavily indebted, extra insurance proceeds may be necessary either to carry the properties until they’re sold, or even to pay off existing indebtedness to free up cash flow for income.

You may even need additional funds if you are taking care of an extended family member, like an aging parent.

These are just some of the many possibilities of expenses that will need to be covered by insurance proceeds.

Before we move on to specific life insurance quotes, let’s first consider the factors that affect term life insurance premiums.

This is typically the single most important premium factor. The older you are, the more likely you are to die within the term of the policy.

This is a close second and why it’s so important to apply for a policy as early in life as possible. Premium rates literally increase by each year.

If you have any health conditions that may affect mortality, such as diabetes or hypertension, your premiums will be higher. This is another compelling reason to apply while you are young and in good health.

It’s not that policies are not available to people with health conditions, it’s just that they’re less expensive if you don’t have any.

A 10-year term policy will have a lower premium than a 20-year term policy, which will be lower than a 30-year term. The shorter the term, the less likely it is the insurance company will have to pay a claim before it expires.

Size of the policy matters, but not the way you might think.

Yes, a $1 million policy will cost more than a $500,000 policy. But it won’t cost twice as much.

The larger the policy, the lower the per-thousand cost will be.

When the size of the death benefit is considered, the larger policy will always be more cost-effective.

For example, certain occupations are more hazardous than others (think policeman versus librarian). Deep-sea diving is higher risk than golf. And smoking is the one activity guaranteed to raise your premiums substantially.

With this information in mind, let’s get onto the term life quotes.

Any discussion on life insurance should include a comparison of whole life and term life insurance coverage. After all, both products can be immensely valuable in the right situation, yet one product (whole life) costs considerably more than the other.

Most of the time, the debate is settled in favor of term life insurance based on cost alone. After all, a whole life insurance policy can easily cost 10x the same amount of coverage you can get with a term policy.

With that being said, whole life insurance and other investment-type life insurance coverage can be valuable in terms of the cash value you can build up over time. Whole life insurance also offers a fixed benefit amount for your heirs that will last for your entire life, yet the cost of your premiums are guaranteed to stay the same.

The cash value of a whole life insurance policy also grows on a tax-deferred basis, and you can borrow against this amount if you need a loan. Further, many whole life policies from reputable providers also pay out dividends during good years, which can be substantial.

The problem with whole life and other similar policies like universal life is the fact that premiums can be exorbitant for the amount of coverage you might need.

A couple with young children provide a good example since they might need a $1 million dollar policy or more to provide income protection for their working years and have money left for college tuition and other expenses.

With young families, expenses are already high.

This includes costs for food for a family, childcare, heavy use of health care, and the seemingly endless demand for clothing, furniture, and even entertainment as the children grow.

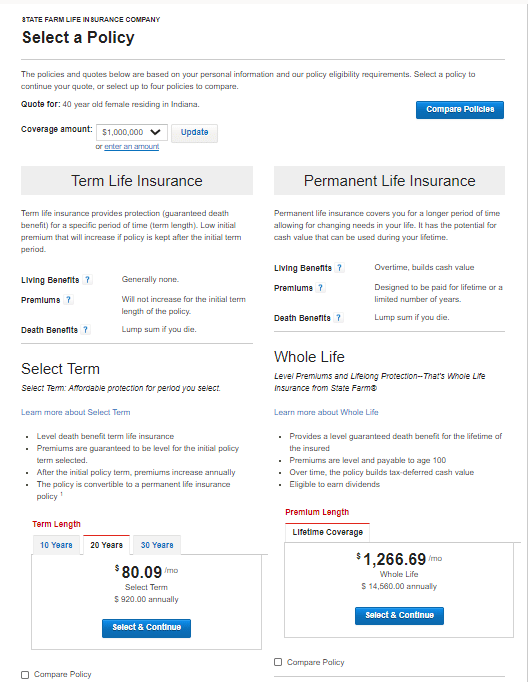

As you can see from the cost comparison below from State Farm, there’s not enough room in the typical family budget to afford the type of life insurance that’s needed. A 40-year-old mother and breadwinner in excellent health would pay $80.09 per month for a term life policy that lasts 20 years, whereas a whole life policy in the same amount would cost $1,266.69 per month (or $14,560 annually).

This is a classic situation where term insurance rides to the rescue. The family can afford to buy the amount of coverage they need at an affordable price, whereas paying for permanent life insurance coverage in the same amount would be difficult to justify.

And just as important for people of any age and in any circumstance, the extra funds not being spent on insurance premiums can be invested to gradually improve your financial situation.

So absolutely, term insurance will work best for most people.

As you’ll notice, each table has a wide array of information. Knowing that everybody is in a different situation, I wanted to make sure that I offered quotes for almost every conceivable situation.

I’ve included quotes for 30-year term, 20-year term, and 10-year term. If you’re a tobacco user, I’ve also included some quotes from life insurance for smokers.

For those that think that a million dollar term policy is expensive, you’ll quickly notice that for a 25-year-old male in good health only costs $645 per year with a 35-year-old costing $795.

On a monthly basis that’s almost next to nothing!

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 25 | MALE | BANNER LIFE $645 | NORTH AMERICAN CO. $645 | TRANSAMERICA $650 |

| 25 | FEMALE | AMERICAN GENERAL $514 | NORTH AMERICA CO. $515 | SBLI $520 |

| 35 | MALE | BANNER LIFE $795 | GENWORTH FINANCIAL $804 | ING $808 |

| 35 | FEMALE | SBLI $640 | AMERICAN GENERAL $694 | GENWORTH FINANCIAL $695 |

| 45 | MALE | BANNER LIFE $1,885 | GENWORTH FINANCIAL $1891 | AMERICAN GENERAL $1,894 |

| 45 | FEMALE | SBLI $1,450 | BANNER LIFE $1,455 | AMERICAN GENERAL $1,456 |

There is a big drop off in price between a 20 year and a 30 year since underwriters do not have to worry as much about life expectancy.

For many people a 20-year policy gets them exactly where they want to be in life when the policy term runs out.

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 25 | MALE | AMERICAN GENERAL $414 | BANNER LIFE $425 | SBLI $440 |

| 25 | FEMALE | AMERICAN GENERAL $354 | SBLI $360 | BANNER LIFE $365 |

| 35 | MALE | SBLI $450 | BANNER LIFE $455 | NORTH AMERICA CO. $485 |

| 35 | FEMALE | SBLI $390 | AMERICAN GENERAL $404 | BANNER LIFE $405 |

| 45 | MALE | BANNER LIFE $1,155 | SBLI $1,160 | GENWORTH FINANCIAL $1,173 |

| 45 | FEMALE | SBLI $880 | BANNER LIFE $895 | TRANSAMERICA $930 |

Once again, you get a $200 drop in the annual premium by losing another 10 years on the term.

If your life insurance agent isn’t giving you all these term options and is only focused on the death benefit, then you need a different agent.

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 25 | MALE | SBLI $260 | BANNER LIFE $285 | MINNESOTA LIFE $290 |

| 25 | FEMALE | SBLI $230 | BANNER LIFE $245 | ING $248 |

| 35 | MALE | SBLI $270 | BANNER LIFE $295 | MINNESOTA LIFE $300 |

| 35 | FEMALE | SBLI $240 | BANNER LIFE $255 | ING $258 |

| 45 | MALE | BANNER LIFE $585 | TRANSAMERICA $630 | GENWORTH FINANCIAL $637 |

| 45 | FEMALE | SBLI $520 | BANNER LIFE $525 | ING $528 |

For all you smokers out there – beware! The cost of your life insurance balloons as you’ll see here. If you’re considering kicking the habit, now is as good time as any.

Some life insurance companies will give you a lower rate if you complete a recognized smoking cessation program, and you go without smoking for at least two years.

It won’t help your immediate situation, but when you see the premium rates below, you might agree that it’s something to work toward!

| AGE | SEX | COMPANY 1 | COMPANY 2 | COMPANY 3 |

|---|---|---|---|---|

| 35 | MALE | North American Co. $3595 | SBLI $3630 | MetLife $3639 |

| 35 | FEMALE | North American Co. $2555 | Transamerica $2720 | Prudential $2765 |

Getting a one million-dollar term life insurance policy is not as expensive as most people believe. You can start getting quotes today from a variety of top life insurers by selecting your state from the map above.

Even those who opt for the more expensive permanent life insurance policy will many times be surprised at the price.

Either way, you can get these larger amounts of coverage and still not break the bank. But get your policy now, while you’re still young and in good health.